Quick Note: We love helping you get behind the wheel, but please remember: we’re car experts, not financial attorneys. This info is to help you learn, but your results may vary! [See full disclaimer below

Welcome back to the Sole Savers Auto Sales weekly credit guide! Last week, we talked about why credit is your financial reputation and how it can save you thousands of dollars on your next car.

But knowing why it matters is only half the battle. To actually change your score, you have to understand the "ingredients" that go into it.

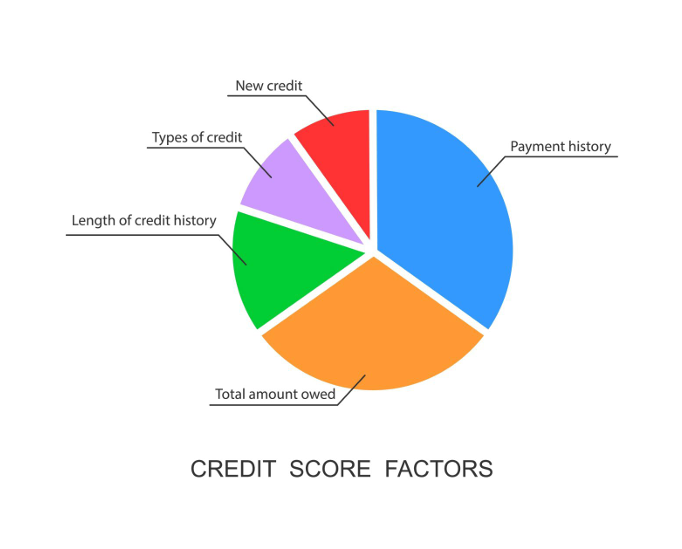

Imagine your credit score is a pie. If you leave out the flour, the pie collapses. If you add too much salt, it tastes terrible. Your credit score is the same way—it’s made of five specific "ingredients," and some are much larger than others. If you want a score that gets you the keys to that dream truck or SUV, you need to know which slices of the pie to focus on first.

1. The Big Slice: Payment History (35%)

This is the most important part of the pie. It accounts for 35% of your total score.

When a bank looks at your credit, the very first thing they ask is: "Does this person pay their bills on time?" This includes credit cards, student loans, personal loans, and even some utility bills.

- The Good: Every time you pay a bill by the due date, you are adding "points" to this category.

- The Bad: A single payment that is 30 days late can knock 50 to 100 points off your score almost instantly.

The Sole Savers Advice: If you can only do one thing this month, make sure every single payment is on time. Set up "Auto-Pay" for your minimum payments so you never have to worry about a slip-up.

2. The "Balance" Slice: Amounts Owed (30%)

This slice is nearly as big as the first one, accounting for 30% of your score. This looks at how much debt you have compared to your credit limits.

This is often called Credit Utilization. For example, if you have a credit card with a $1,000 limit and you have a $900 balance, your utilization is 90%. Banks see this and think, "This person is stretched too thin. If they buy a car today, will they be able to afford the gas and insurance?"

The Goal: Try to keep your balances below 30% of your limit. On that $1,000 card, you’d want to keep the balance under $300.

3. The "Experience" Slice: Length of Credit History (15%)

Think of this like a job resume. If you see a resume with 10 years of experience, you trust that person more than someone who started yesterday.

Credit works the same way. This 15% of your pie is based on how long your accounts have been open. The older your accounts are the better.

Common Mistake: People often close old credit cards they don't use anymore thinking it will "clean up" their report. Don't do this! Closing an old account makes your credit history look shorter, which can actually drop your score.

4. The "Variety" Slice: Credit Mix (10%)

Banks like to see that you can handle different types of money. There are two main types:

- Revolving Credit: Like credit cards (where the balance goes up and down).

- Installment Credit: Like a car loan or a mortgage (where you pay a fixed amount every month).

If you have a healthy mix of both, it shows you’re a well-rounded borrower. If you only have credit cards, adding a small installment loan (like a car loan from us!) can actually help this part of your pie.

5. The "Newbie" Slice: New Credit (10%)

Every time you apply for a new loan or credit card, a "Hard Inquiry" is placed on your report. This makes up the final 10% of the pie.

If you apply for ten credit cards in one week, it looks like you’re in a financial emergency, and your score will drop. However, "shopping" for a car loan is different—the credit bureaus usually count multiple inquiries for a car as just one "hit" as long as they happen within a short window (usually 14–45 days).

Why This Matters for Your Next Car

When you walk into Sole Savers Auto Sales, we want to get you the best deal possible. By understanding this pie, you can start making moves today that will pay off when you're ready to buy.

- Focus on the big slices first: Don't worry about "New Credit" (10%) if you’re still missing payments (35%).

- Pay down those cards: If you have some extra cash, putting it toward a credit card balance is one of the fastest ways to see your score jump up.

Putting It Into Practice

You don't have to fix everything overnight. Credit repair is a marathon, not a sprint. This week, we want you to look at your "Big Slice." Are you paying your bills on time? If not, what is one bill you can put on Auto-Pay today

At Sole Savers, we’ve seen people go from "No" to "Yes" just by making a few small adjustments to their Credit Pie. We’re here to help you understand those ingredients so you can get the recipe for success.

Next Week: We’re going to get practical. We’ll show you exactly where to go to get your credit report for FREE (without getting scammed) and how to read it like a pro.

- 35% Payment History (Blue): The "Big Slice."

- 30% Amounts Owed / Credit Utilization (Green): The "Balance Slice."

- 15% Length of Credit History (Orange): The "Experience Slice."

- 10% Credit Mix (Purple): The "Variety Slice."

- 10% New Credit (Red): The "Newbie Slice."

Disclaimer: Sole Savers Auto Sales is a motor vehicle dealership, not a credit repair organization, tax advisor, or legal firm. The information provided in this 52-week series is for educational and informational purposes only and does not constitute legal, financial, or professional advice. Credit scores are impacted by numerous factors, and results from the strategies discussed may vary based on individual credit profiles. We do not guarantee any specific increase in credit scores or loan approvals. For specific advice regarding your financial situation, please consult with a certified financial planner or a qualified legal professional